Have you received a notice from your insurance company that your rates will increase, or worse, your coverage will be terminated, because of the state of your roof?

Many home insurance companies deem a roof that’s 20+ years old “uninsurable,” but in addition, other factors such as the shape of your roof, materials used, and geographic location can impact your premiums.

So, if you are questioning if replacing your roof will lower your home insurance premiums, the answer is most likely “yes.” Homeowners can realize a 5-35% reduction in insurance premiums with a new roof (the national average hovering around 20%).

TL;DR - Quick Takeaways

A new roof can reduce your homeowners insurance premiums by 10–20% or more if it’s impact-resistant, wind-rated, or properly certified. Roof age, materials, shape, and location can all influence your insurance cost.Voluntary upgrades often qualify for discounts, while damage claims may temporarily raise premiums.

Maintenance, documentation, and choosing a qualified, licensed roofer are key to keeping discounts active.

Why Roof Condition Plays a Big Role in Homeowners Insurance

Insurance companies see your roof as one of the biggest indicators of risk. It’s your home’s first line of defense, so a roof in good shape helps reduce the likelihood of leaks, wind issues, and water damage — the kinds of problems that can result in expensive claims and can impact your insurance premiums.

Visible wear increases perceived liability. Missing shingles, damaged flashing, or general aging may lead insurers to adjust your policy with higher costs or limited coverage.

Age matters. Once a roof hits 15–20 years old, even small signs of deterioration can raise concerns during policy renewals. Keeping up with proper maintenance shows that your home remains a low-risk investment.

How Your Roof Affects Your Home Insurance

Several factors determine how your roof affects homeowners insurance rates.

Insurers look at roof types for insurance, including the materials used and how well they protect against severe weather.

Roof shape also impacts wind and water performance. Local climate adds another layer of risk, influencing the likelihood of damage and future claims.

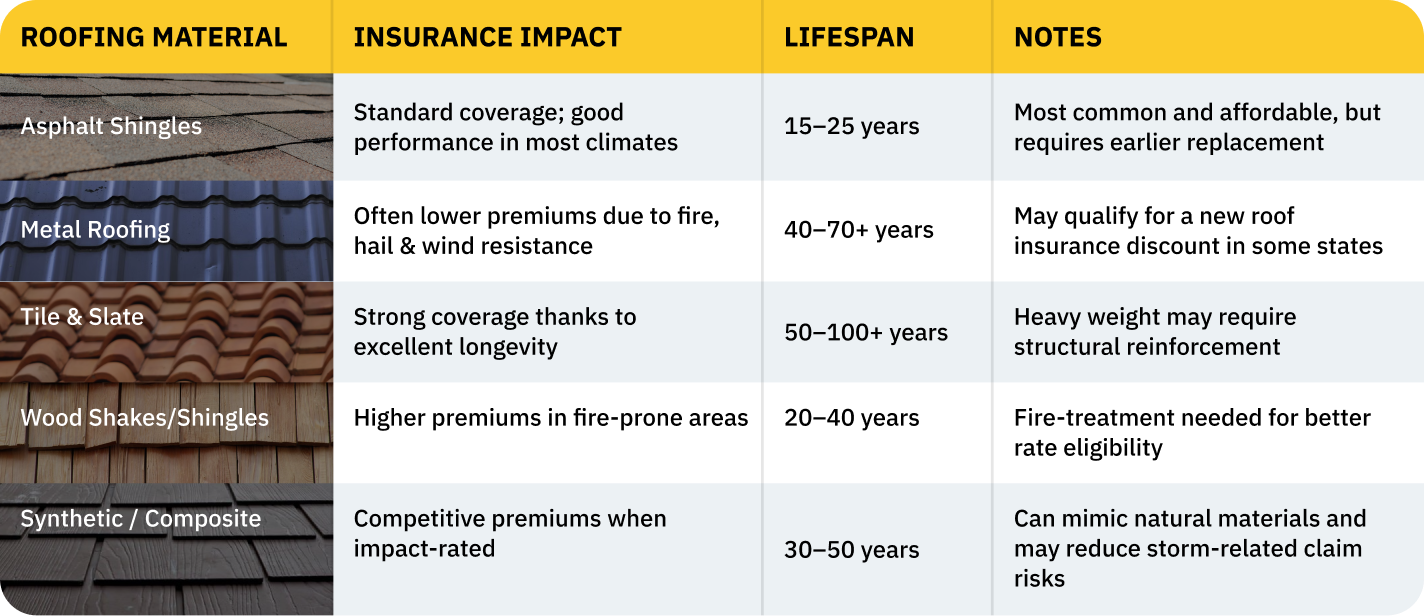

Roof Material Types

Understanding roof material types for insurance helps you choose a roof that performs well in your region’s weather and supports the best possible policy pricing. Insurers look at durability, fire resistance, and storm protection — qualities that can influence whether you qualify for a new roof insurance discount.

Opting for a Class 4 impact-rated roof can help protect your home from hail and debris while also signaling to your insurer that your roof is less likely to generate a claim.

Learn more about choosing roofing materials

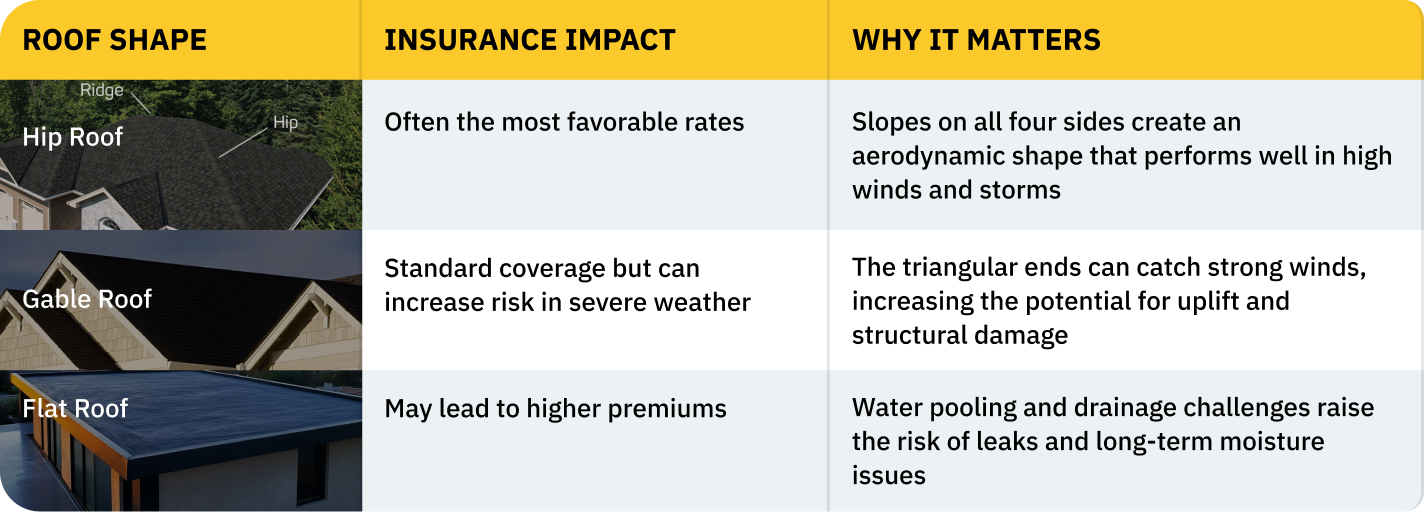

Roof Shape and Design Considerations

The shape and structural design of your roof also affect how insurers evaluate risk. Some designs hold up better in heavy wind and rain, while others are more prone to leaks or structural stress. Understanding common roof shapes for insurance can help you make a smarter choice whether you’re planning a roof replacement or a new build.

Upgrades can make a big difference. Features like Secondary Water Resistance (SWR) barriers, reinforced roof decking, or metal connectors between the roof and walls help reduce storm-related damage and improve policy eligibility. In states like Florida, wind mitigation programs reward these strengthened designs with lower premiums. See: Installing a Windproof Roof, Storm-Proofing Your Roof

How Local Climate and Location Affect Your Rates

Where you live plays a huge role in how your roof affects your home insurance. Weather patterns and environmental risks shape not only the level of protection your roof needs, but also how insurers price your coverage. That’s why two similar homes can have different premiums.

After major storms, seasonal snow, or wildfire exposure, it’s crucial to inspect your roof early to keep minor issues from becoming expensive claims.

By choosing roofing materials built for your local climate, you not only reduce long-term damage but may also qualify for a new roof insurance discount tailored to weather risks in your state.

Voluntary Replacement vs. Insurance Claim Replacement

How you approach a roof replacement — voluntarily or through an insurance claim — can impact both your coverage and what you pay for homeowners insurance.

Voluntary roof replacement happens when you choose to upgrade before significant damage occurs — often for better durability, energy performance, or appeal. Because this is a proactive step that helps prevent future claims, insurers sometimes offer a new roof insurance discount or more favorable coverage terms (see Benefits of a Well-Maintained Roof).

Insurance claim replacements occur after major storm, hail, or fire damage. While your policy may cover the cost, the claim becomes part of your insurance history. Too many claims within a short time can raise premiums and lead to higher deductibles (see How to Make Roofing Insurance Claims for Storm Damage).

If you believe weather may have caused damage, proper inspection matters. Understanding documentation, adjuster evaluations, and payout options can save you stress and money — our detailed walkthrough in Roof Insurance Claim Process: Step-by-Step Guide explains what to expect.

Frequently Asked Questions

BLOG

Premier Roofing & The Press

Top Roofing Companies in Wichita: 2026 Guide

A lot of homeowners in Wichita end up replacing their roof sooner than expected, not because it was necessary, but because the damage wasn’t properly assessed early on. It happens more often than people think. If you’re searching ...

9 Best Roofing Companies in Kansas City: 2026 Guide

Most people don’t search for the best roofing companies in Kansas City until something goes wrong. A leak shows up after a storm. Shingles end up in the yard

How to Choose a Roofer in St. Louis

Finding the right roofer isn’t just a box to check off. It’s one of the most important decisions you’ll make as a homeowner in St. Louis. Between Missouri’s unpredictable storms, intense summer heat, and strict local codes, your roofing system needs more than just an ordinary contractor. Your roof needs a proven expert. One poor roofing installation or missed code compliance can result in expensive repairs, water damage, or insurance claims down the road.